Stop Comparing Argentina's Rent Control to Rent Stabilization in the United States

Argentina’s President Javier Milei is a libertarian darling who abolished rent control by decree in late 2023 upon taking office. The number of available rental units shot up about 150 percent according to some sources and rents declined substantially in real terms. Some have asserted that abolishing rent control presents a blueprint for US cities to substantially increase the stock of rental housing and bring down rents. Alas, Argentina’s experience is due to key differences in how its housing policy interacted with its unstable economy. The Argentine experience offers little insight for policy makers in the states.

How Binding?

Rent control in the United States rarely acts as a price cap or hard ceiling on rents. Rather, rent increases are usually capped by statute according some formula which takes inflation into account. Alternatively, like in New York City, allowable rent increases are set by a board. Nearly universally, newly built housing or existing housing built after a certain year is exempted. This group of policies which do not cap rent but do cap increases are frequently referred to as rent stabilization.

The strength of the effect of rent stabilization on the rental market market depends on how binding it is. That is, how likely is the cap on increases to be triggered, and how much would the market increase in rents exceed the cap were it not in place. A cap of 15 percent on rent increases in the United States would have almost no effect on the rental market. Rents rarely if ever rise this much in a single year. When President Joe Biden proposed a rent stabilization scheme of 5 percent plus the rate of inflation according to the Consumer Price Index, it set the internet ablaze. However, in a vacuum, this policy would do little to affect the housing market. Again, rents very rarely rise more than five percent above inflation. Most multifamily feasibility studies, be they ground up development or acquisitions, project rent growth of 3-5 percent in nominal terms, that is, not adjusted for inflation. Inflation plus 5 percent far exceeds that.

Lastly, when caps consistently bind rent hikes, even when the market rate increases (which is usually just closely tied to inflation) exceeds it only by a small amount, the effects can be large over time because of compounding. Say an apartment rented for $300 per month in 1980. If rent control capped increases to 1 percent, it would rent for only $470 dollars today. If it were allowed to increase at roughly the rate of inflation of 3.1 percent over that time period, the rent would be $1135. If we assume that operating expenses were 30 percent of rents, a typical benchmark in the industry, the cost to operate this unit would be $340 a month, while if it fell under rent control, it would only rent for $470. This means that the rent controlled unit is barely profitable, and if rents continued to rise faster than costs in the coming years, taking it off the market may be more profitable to than renting it out.

Argentina’s Rent Stabilization

In 2020, Argentina passed a sweeping rent stabilization bill which made big changes to the regulatory framework.

It indexed rent increases to inflation and wage growth, giving 50 percent weight to each

It mandated three year leases, though rents could be adjusted once per year according to the above rule

It mandated that contracts be denominated in Argentine Pesos

It mandated that all landlords register they properties and leases with the government or face fines

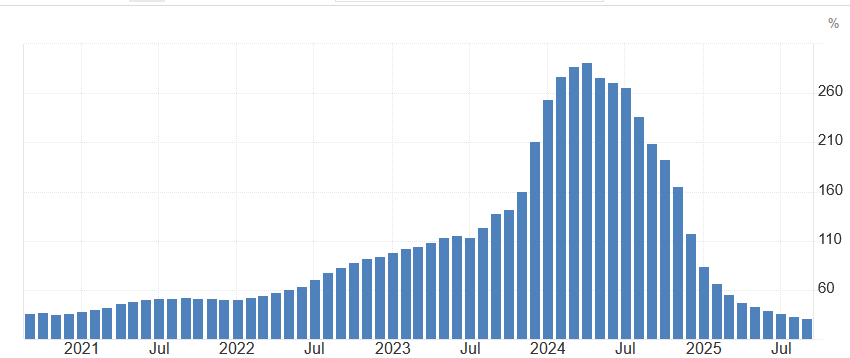

These rules all had a big effect on the rental market in important ways. First, Argentina’s inflation rate has run between 35 and 260 percent since 2020. Allowing rents to only be increased once a year means that a substantial part of the rent is lost to inflation during the year before rents can be adjusted.

Second, because of the sky high inflation, many landlords denominated leases in US dollars since the Peso loses a significant portion of its real value every month due to nosebleed inflation. The law banned this practice, which in effect further capped rents due to high inflation. It also strongly incentivized landlords to list properties on short term vacation rental platforms like AirBnB where customers pay in US dollars and thus landlords are protected from triple digit inflation.

Lastly, Argentina’s tax collection is incredibly lax and the increased enforcement of tax collections on landlords by forcing them to register with the government reduced after tax returns, since many landlords simply did not report rental income to the tax authorities. Under the new law, they risked significant penalties for not registering their properties (and not paying taxes).

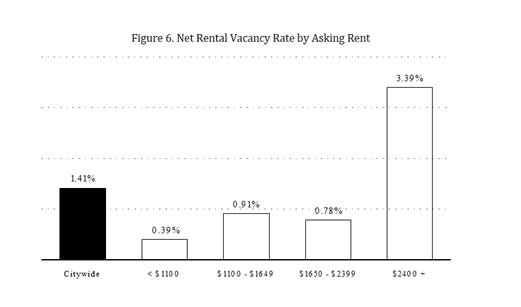

All these factors made Argentina’s rent stabilization significantly more binding than most forms of stabilization in the United States. Indeed, in Argentina, it was estimated that 1 in 7 apartments were vacant after the new rent stabilization law passed. In New York City, where close to 40 percent of rental housing is stabilized, the vacancy rate is less that 1.5 percent, and the vacancy rate for the cheapest units, which are virtually all stabilized is less that 0.5 percent.

Thus, lifting rent control is unlikely to see a flood of vacant units hit the market like in Argentina. Rather, in places like New York City and San Fransisco, ending stabilization would likely just result in mass displacement of rent stabilized tenants.

To be sure, many cities with large stocks of rent stabilized units must address the issue of apartments getting pulled from the market when they require costly upgrades to make habitable again, usually when damaged by a tenant, and allowable rents do not let owners recover those costs. However, this situation affects a tiny percentage of the rental stock in most cities.

Conclusion

Argentina’s rent stabilization law was far reaching, affected all rental housing (not just that built before a certain year), and ended up capping rents significantly below Argentina’s hyperinflation by allowing only for a single adjustment every year, and banning contracts denominated in US dollars. Most rent stabilization in the United States is far more moderate and thus does not result in a significant number of units being kept off the rental market. There is relatively little US policy makers can learn from Argentina’s experience when in comes to rent decontrol.